- The Hivemind Brief

- Posts

- Hivemind Brief 005 | Liquidity reignites, gold leads, and Bitcoin enters its balance-sheet era

Hivemind Brief 005 | Liquidity reignites, gold leads, and Bitcoin enters its balance-sheet era

+ Dmitri Cherniak Feature, AVAX One Launch, and New Podcast with Blueprint

Welcome back to The Hivemind Brief!

A packed edition as Q4 unfolds: liquidity is back, scarce assets are rising, and digital assets are finding their footing.

In this issue: Central banks signal the end of tightening as gold breaks all-time highs, Bitcoin transitions from speculation to reserve, and the new class of Digital Asset Treasuries (DATs) begins to take shape.

Plus: Dmitri Cherniak’s generative works within our Digital Culture Fund, Hivemind leads AVAX One’s $550M capital strategy, and our latest podcast episode with Blueprint’s Jake Greenstein on how operational rigor defines real edge.

From Richard Skeet, Managing Partner and Head of Research

“Earnings don't move the overall market; it's the Federal Reserve Board... focus on the central banks, and focus on the movement of liquidity... most people in the market are looking for earnings and conventional measures. It's liquidity that moves markets.” — Stanley Druckenmiller.

The money printer never truly stops - it just changes forms. As we enter the final quarter of 2025, markets are navigating a remarkable confluence: central banks easing into slowing growth, gold surging to all-time highs, and risk assets benefiting from what remains an extraordinarily liquid environment. The Federal Reserve’s recent rate cuts and signals that quantitative tightening may soon end reveal tightness in the financial system's plumbing - even as headlines celebrate resilient growth. This is the environment where monetary debasement hedges historically thrive, and we expect digital assets to follow gold's trajectory as this dynamic unfolds.

Gold has rocketed past $4,200, with silver testing its 1980s peak of $53.60 - moves of this magnitude typically don't happen in isolation. This meteoric rise tells a clear story: global capital is rotating toward scarce, non-dilutable stores of value. For the first time, central banks now hold more gold than U.S. Treasuries as a share of foreign reserves (a directionally correct view, although there is some debate) - a quiet but profound vote of no confidence in sovereign debt sustainability. While gold has run hard, Bitcoin and digital assets have yet to fully respond. History suggests this lag won't persist. When concerns about monetary debasement drive traditional safe havens, digital alternatives are expected to follow with force.

Last weekend's crypto market turbulence - nearly $19 billion in liquidations across a matter of hours - offered a stark reminder that digital assets have a habit of speed-running financial history. The mechanics were familiar to any student of market structure: overleveraged positions, cascading margin calls, and liquidity assumptions that evaporated under stress. Auto-deleveraging mechanisms embedded into the standard derivative contracts forced counterparty losses onto profitable traders, amplifying the chaos. Yet there's little genuinely new here - just the same dynamics that have plagued traditional markets for centuries, compressed into a weekend. The lesson, as always: capital transfers from the impatient to the patient. Those with conviction and appropriate positioning weather these storms; those chasing leverage with insufficient buffers do not. This wasn't a crisis of fundamentals - it was a reminder that the continuous pricing and infinite liquidity assumption that underpin many models are comfortable fictions, not market realities.

Meanwhile, traditional markets are flashing late-cycle signals that warrant attention. The IPO market is red-hot, and JPMorgan and Goldman just landed the largest LBO in history: a $55 billion take-private of Electronic Arts. Recent credit events - First Brands' automotive parts business and Tricolor, a US subprime lender - underscore growing stress in levered corners of the market. These are classic markers of froth and fragility. Yet dismissing the cycle as purely speculative misses a critical element: unlike previous late-cycle manias built on financial engineering alone, this one has a tangible infrastructure foundation. AI capital expenditure is very real. The infrastructure build-out from hyperscalers represents a multi-hundred-billion-dollar "pig in the python" - private sector stimulus that will flow through to GDP in the coming quarters.

That said, the AI boom carries its own risks. US equity concentration is extreme: the top 10 companies represent nearly 40% of total market cap, with Nvidia increasingly critical to the entire AI ecosystem. Beyond concentration, circular financing raises eyebrows - Nvidia's $100 billion OpenAI deal, Oracle's data-center arrangements, and the web of cross-investments linking Microsoft, OpenAI, and Google suggest interdependencies that could amplify stress when the cycle turns. Add concerns about GPU asset depreciation, cheaper AI alternatives coming out of China, like DeepSeek, and mixed productivity evidence, and the picture becomes more complex. This isn't financial engineering in the traditional sense, but neither is it risk-free infrastructure spending.

Our view: extended, but supported. Yes, we're closer to a blow-off top than the nadir of the last cycle. Credit stress is emerging, concentration risk is real, and late-cycle excesses are visible. But with the Fed easing, liquidity ample, and structural capex driving near-term growth, this environment can run longer than skeptics expect. For digital assets, the setup remains constructive: gold leading the way, system liquidity improving, and adoption infrastructure maturing. The flush last weekend cleared leverage and reminded us that volatility is the price of admission. For those with conviction, these moments aren't warnings to exit - they're invitations to lean in.

The Next Phase of Bitcoin

Bitcoin’s role in the financial system is shifting from speculative asset to structural reserve. In Q2 2025, the number of corporate and institutional holders surpassed 250, together owning over 930,000 BTC (≈4.4% of supply). What began as a hedge against inflation has evolved into a balance-sheet reserve held by corporates, endowments, and even sovereign entities.

At Hivemind, we see this as the rise of a new class of market participant: Digital Asset Treasuries (DATs) — public companies accumulating crypto as core holdings. With over 75+ opportunities screened and 10+ investments to date, we’re actively helping define this new frontier in on-chain finance.

Read: Bitcoin’s Great Repricing - A Macro Asset Finds Its Place

by Richard Skeet, Managing Partner and Head of Research

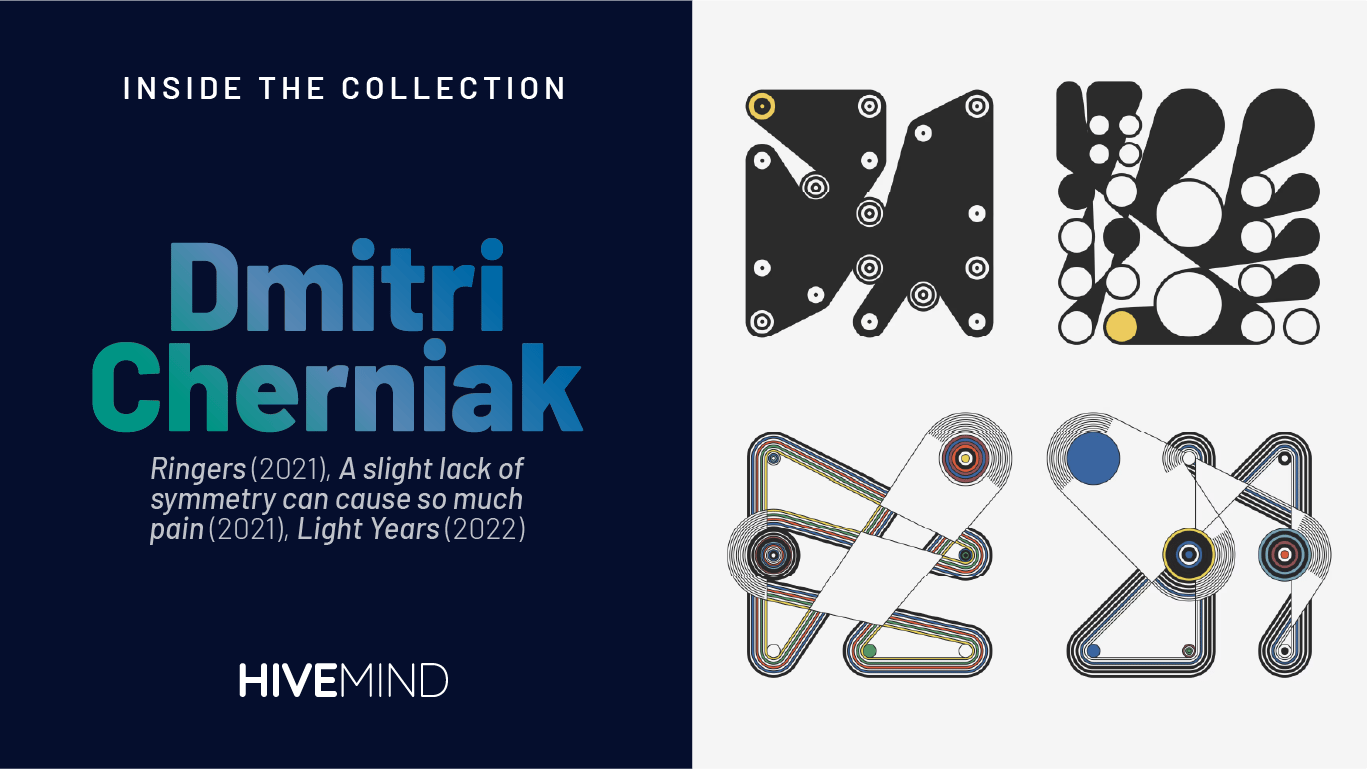

Into the Collection: Dmitri Cherniak

Dmitri Cherniak holds a central place within the Digital Culture Fund’s collection, which includes Ringers, A slight lack of symmetry can cause so much pain, and Light Years. His practice bridges analog art traditions like Constructivism and Dada with the autonomy and emergence of on-chain algorithms - embodying the very intersection of art and code that defines generative art’s enduring legacy.

In our latest feature, we explore the collections without our fund and examine how these acquisitions illustrate our long-term conviction in the cultural and institutional relevance of generative art.

Read: Inside the Collection: Dmitri Cherniak | Ringers (2021), A slight lack of symmetry can cause so much pain (2021), & Light Years (2022)

Hivemind Leads $550M Capital Strategy for AVAX One

Hivemind Capital Partners is proud to lead the launch and $550 million capital strategy for AgriFORCE, to be renamed AVAX One, the first NASDAQ-listed company dedicated to the Avalanche ecosystem. Built to provide institutional investors with pure-play, regulated exposure to AVAX, AVAX One represents a major step toward bridging traditional capital markets and on-chain finance.

As lead investor and nominated Chairman of the Board, Hivemind Founder Matt Zhang describes the company’s vision as “building the Berkshire Hathaway of the on-chain financial economy” a multi-year thesis that reflects our conviction that programmable blockchains like Avalanche will serve as the new foundation for institutional-grade financial infrastructure.

Read the full press release and follow AgriFORCE on X and Linkedin for further updates.

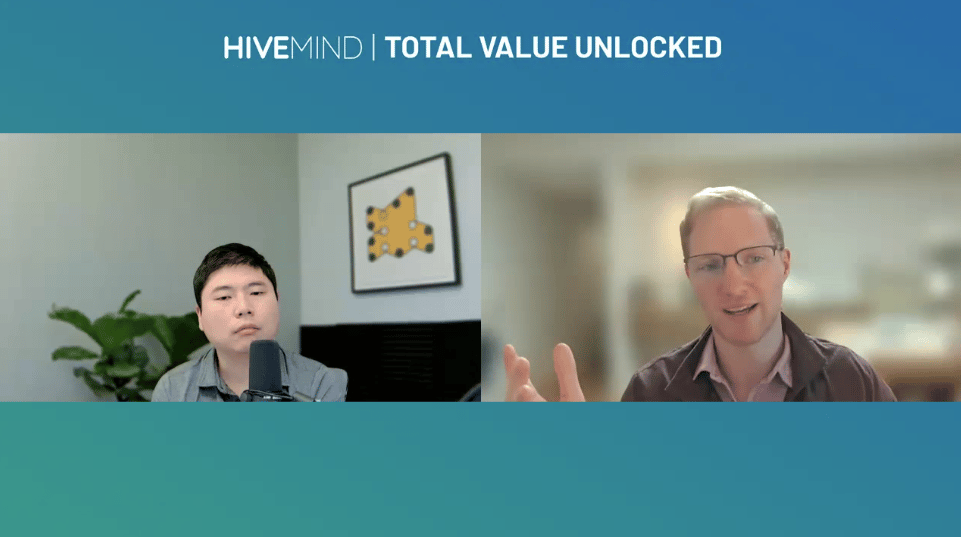

Operations as your edge with Blueprint

In our latest Total Value Unlocked episode, Matt Zhang sits down with Blueprint CEO Jake Greenstein to unpack the operational backbone of digital asset management and why the real edge often lies beneath the surface. Together, they discuss risk management, staking infrastructure, and the evolution of Blueprint, a unified orchestration platform built by operators, for operators.

Watch the full episode here or anywhere you listen to your podcasts.

We’re Hiring!

Open Hivemind Positions:

More roles within our network here!

DISCLAIMER: All views expressed are Hivemind’s own views. The information provided herein has been produced and issued by Hivemind Capital Partners UK LLP (“Hivemind”) and is being provided for informational purposes only. This document is not to be distributed or reproduced in any way. This document does not constitute or contain an offer to purchase or sell securities. This document is confidential and intended for the person to whom this was delivered. If you have not received this document from Hivemind you are hereby notified that you have received it from a non-authorized source and you are prohibited from reading, using, retaining, disseminating or copying this material without the prior express written consent of Hivemind. Neither Hivemind nor any of its affiliates or representatives makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein or any other written or oral communication transmitted or made to the recipient. The information contained in this document is current as of the date indicated, and Hivemind undertakes no obligation to update, modify or amend this document or to otherwise notify a reader in the event that any matter stated herein changes or subsequently becomes inaccurate.

This document has not been compiled, reviewed, or audited by an independent accountant. Past performance should not be construed as an indicator of future results, and there can be no assurance that historical trends will continue. This document does not include information regarding each investment or investment strategy pursued by the Funds. References to investments included herein should not be construed as a recommendation of any particular investment.

Certain information contained herein may constitute “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof, other variations thereon or comparable terminology. All such forward-looking statements are solely statements of opinion, and there is no assurance that they will be predictive of actual events.